As inflation is a very hot topic in the mid of 2021, we've seen the FED saying, ‘this inflation we're seeing now is short term, and there is nothing to worry about’, on the other hand we've seen Warren Buffett talking about how he's seeing big inflation throughout Berkshire Hathaway's businesses. We've also got Michael Burry making a new big-short on bonds.

So how does high inflation affect the investors and what's the best way to deal with a period of high inflation?

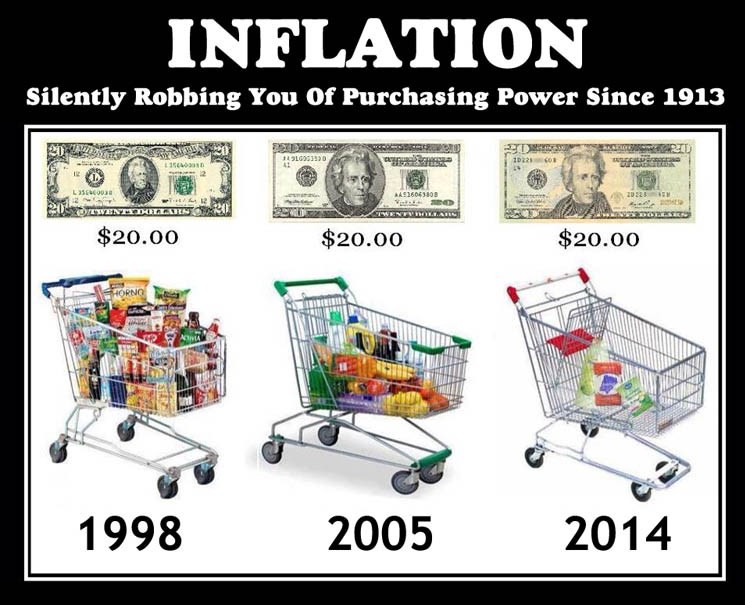

All the investors want to do is - commit a certain amount of money to an investment and get more money back at some point in the future. But when we talk about inflation and investing it's more helpful to think of investing like - giving up a certain amount of buying power now, to have more buying power in the future. Like giving up the purchasing power to buy 100 apples now in the hope that we have the purchasing power to buy 150 in the future

While you may make a 20% gain on an investment on paper over a few years if inflation is running rampant, there's a potential that your real return is zero. E.g. you could buy 100 apples before, then you make 20% on your, investment then you sell it, but after that you can still only buy 100 apples now. You've had no gain in purchasing power.

This is what Warren Buffett talked about in 1979. He said that a business with per-share net worth compounded at 20% annually, would have guaranteed its owners a highly successful real investment return, but now such an outcome seems less certain for the inflation rate coupled with individual tax rates will be the ultimate determinant as to whether our internal operating performance produces successful investment results.

It is just as the original 3% savings bond, a 5% passbook savings account, or even an 8% US treasury note have in turn been transformed by inflation into financial instruments that chew up, rather than enhance purchasing power over their investment lives

A business earning 20 on capital can produce a negative real return for its owners under inflationary conditions not much more severe than what presently prevail. And this was in 1979 and the inflation rate was 11%.

Buffett says the combination of the inflation rate plus the percentage of capital that must be paid by the owner to transfer into his own pocket the annual earnings achieved by the business, i.e ordinary income tax on dividends and capital gains tax on retained earnings - can be thought of as an investor's misery index when this exceeds the rate of return earned on equity by the business the investors purchasing power real capital shrinks even though he consumes nothing at all.

Inflation is a crummy time for investors because when you take into account its rate - you can think about the annual percentage loss of purchasing power. If you couple that with either taxes you have to pay on income received through dividends and the capital tax the capital gains tax you have to pay when you sell then your real return on your investment could be negative even if the business is going well.

In 1980 Warren Buffett made the following analogy ‘the average tax paying investor is now running up a down escalator which pace is accelerated to the point where his upward progress is nil.’

And even if you are not an investor inflation can be a crappy time for businesses as well. Inflation eats away at the purchasing power as well and businesses generally need to buy a lot of stuff to keep operating. And if this stuff is now all of a sudden more expensive, they're trapped in a dilemma either they pay the higher price to operate, therefore making less profit or they raise the prices (produce more inflation) and hope that their sales volume doesn't shrink.

Inflation can also put upward pressure on interest rates which can make it harder for companies to access loans or make pre-existing loans more expensive to pay off, and this makes it much harder for the investor to pick great stocks that are going to compound money over time.

Warren Buffett explains what type of businesses tend to do well even in periods of high inflation. Such favored business must have two characteristics:

1. An ability to increase prices rather easily even when product demand is flat and capacity is not fully utilized, without fear of significant loss of either market share or unit volume

2. An ability to accommodate large dollar volume increases in business often produced more by inflation than real growth with only minor additional investment of capital

So, on the first one - an ability to increase prices and face no consequences. The business is feeling higher costs which hurt their margins so why not push those extra costs onto the customer if they can.

And you may think –‘ that is ridiculous, no company could do that, and the customers would just go and buy the cheaper product elsewhere, but not if the company has a moat.

If you're a small production company you've spent money to train all 50 of your employees to use Photoshop and Premiere pro and After effects - that took time, and it took money. Adobe suddenly decides to up the subscriptions ten dollars more per month.

Your company management might be thinking – ‘let's switch to a cheaper alternative, maybe you find a cheaper alternative, twenty dollars a month cheaper, great but it doesn't have all the same features as what the team's already using. Plus, it's going to cost two hundred dollars per employee to train them on the new software, not to mention the downtime your business will experience to get that training done and to switch everybody over.

If you think about the clients - they are already stressing you out, they're trying to get their productions finished, and at the end of the day it's just not worth switching. So, what can you do? You just pay the increased subscription, and you stick with Adobe, and pay more.

Another example: Apple has such a strong brand mode and a strong ecosystem that it's completely normal for them to squeeze a little bit more, and a little bit more out of all their customers each year.

In 2012 iPhone average selling price was just over $600. At the end of 2018, it was almost $800. Nowadays, it's even higher, and that's not even considering the plethora of add-on subscriptions. Apple will somehow force upon you whether it be AppleCare or iCloud or Apple Music, there's no escape and that's the point. So, during inflationary times look to the companies with very strong moats which can raise prices without consequences.

Secondly, you want the business to have an ability to accommodate large dollar volume increases in business with only minor additional investment of capital. So, if your business is not just able to pass on extra costs to the consumer, that means that you're going to have to cope with those costs, which means lower margins to generate your profit. It means you need to be able to increase the amount of business you're doing.

Essentially, what Buffett is saying here is - you want companies that are growing and are also easily scalable. For example - a shipbuilding company would struggle on this point. It costs a lot to build a big ship, you're not going to make huge margins doing it, but it's also very hard to increase the number of ships you're delivering each year. That would take enormous investment, into new shipyards and it'll be slow to wind up.

And if you consider a company like Facebook on the other hand if they can’t pass on the extra cost to their customers (which are the advertisers), they could just choose to bump up the frequency of sponsored posts or of other ads. When a user is scrolling Instagram or Facebook they see three ads, instead of seeing two, and Facebook could do that very easily, and very quickly.

3. And Buffett has one more piece of advice for those seeking the best strategy during a time of inflation. Invest in yourself!

Sometimes there's just no escaping. Stock market investing in these times can be hard, so and given the fact that we're dealing with fairly high levels of inflation what can we do?

To improve your own earning power, know your own talents. Very few people maximize their talents and if you increase your talents, they can't tax it while you're doing it, they can't take it away from you. If you become more useful in your activities your profession - doctor, lawyer, auto repair, etc… - that’s the best protection against a currency that might decline at a rapid rate and the best investment.

And a good passive investment – is an investment in a good business. If you own an interest in a good business, you're very likely to maintain purchasing power no matter what happens to the currency.

Warren Buffett is indirectly acknowledging that it's hard to do well as a stock market investor when inflation just keeps ramping up. It's a bad time and your real return can be zero, so probably a better thing to do is invest in yourself, up-skill so that you can achieve a higher level of income. And your personal buying power would not fall - make yourself more valuable.

Overall, Warren Buffet gives us those 3 invaluable points. Those just come back down to the competitive advantage of you and your business – have a moat, be able to scale quickly and cheaply, and the last one is to invest in yourself.