Jeremy Grantham is a co-founder and chief investment strategist of Boston’s GMO. Jeremy believes that in 2021 - U.S. stocks have become an epic bubble and will burst so badly to outshine the crashes of 1929 and 2000.

Here is what Jeremy Grantham outlines

1. What happens when the market crashes

I believe that the bull market, started in March 2009, the longest bull market in history, have matured into a speculative fever of rare proportions, a fully-fledged epic bubble. It would be surprising if we have one that long that didn’t end up with animal spirits beginning to freak out a bit.

Achievement like that normally takes a friendly economy and even friendlier FED behavior, but this one managed to do with somewhat wounded economy on a global basis. We even had more spectacular FED and Government friendliness. The usual moral hazard that has been going on since Greenspan arrived the 90s.

The result of that is that confidence has risen and risen and risen until finally people are reaching for the greatest demonstration of confidence, they have had in their investment career. They are borrowing more money to throw it into the market, their belief in the market is profound, the common wisdom is that the FED on your side, how can you lose. And nowadays there appear to be no doubters at all.

The belief is that – all you need is the FED on your side and the stocks will rise forever.

And some of the signs to look for a bubble are, e.g. look at over-the-counter trading. Last Feb it traded about 80mil shares for the month, and it worked its way steadily through the year until Nov, when it was about 380mil. And then in Dec it went to 1.15 trillion shares for the month, having tripled and tripled again in just a month. These are spectacular performances.

My own stock at Quantum scape came into the market at 10 and shot up to 130, and it became bigger than GM or Panasonic. And it is a brilliant company, but it already admitted it won’t be producing any batteries for 4 years. So, no sales, no income for 4 years and yet bigger than GM.

There has been nothing like that in 1929, nothing of that scale. Nothing like that in 2000 either. 1929 run into great depression and global trade problems, so you really want to the first leg down, which was big enough.

The analogy with 2000 is better, and it went down 50% back then. And the reason it went down only 50% and bounced back relatively quickly was because FED came charging into the rescue. And you can have a lot of rescues when you start at a 16% long government bond for example in 1982. You can have a bull market as you go down from 16 to 12 and another bull market from 12 to 8, and 8 to 4.

And now we are down at about 2.5% and you have to realize that most of the easy pickings of saving the game by ramping rates down is behind us. At the lowest rates in history, you don’t have a lot in the bank to throw on the table.

The idea that the real world doesn’t count and all you need is money – to generate real wealth – I am pretty sure most of the people feel it’s an illusion. The situation where we have a deadly virus, and the economy is obviously on its knees and the FED is doing everything it could – and would that be enough to save the system?

In the end the system is about the amount of people working and producing, the amount of capital spending, the quality of education and production of the workforce.

COVID-19 brought spectacular excesses on the part of the FED and the Government writing checks. Unprecedented, and the combination was very powerful.

And the market had the opportunity to crash a couple of times, e.g. in 2018 – the last time. And those bull markets can go on forever. You don’t know how high and how long they could go.

In the back of everyone with bear’s mindset must be surely Japan in 1989. During that time, they managed to get to 65 times the market earnings. It has never previously gone over 25. So, the markets are unpredictable – when we avoid the burst of euphoria.

Tesla is an emblematic as crazy investor behavior. At the same time, anyone who has bet against Elon Musk has lived to regret it so far. Going short is only for experts because you can get into bankruptcy very quickly. My recommendation is to not go short individual stocks.

When you reach such levels of hyper-enthusiasm, the bubble has always, without exception broken in the next few months, not few years.

“You can’t maintain the level of near ecstasy for a long time. It can’t be done because you’ve put in your last dollar. You are all in. What are you supposed to do – beyond that point? Time comes when you can’t borrow any more money and can’t take any more risk.”

How do you keep this level of enthusiasm going indefinitely?

And if the Government is going to write unprecedentedly large checks, then indeed the all-in position can expand one last desperate notch. The sad truth about the so-called stimulus is it didn’t increase capital spending significantly; it didn’t significantly increase the real production. This will lead to an even more spectacular bust.

The flow of dividends and earnings – that’s the only think you can end up eating, and sooner or later the stock market – will once again – sell on the future flow of dividends.

On 23 Mar 20 the FED managed to engineer a revival of the credit market and ultimately a spectacular rebound in stocks. But if we go before COVID you would notice we have already lost considerable power on the economy. We had fewer people working and we had a reduced stream of goods and services.

This is a monetary game, and you can keep these little monetary bubbles going for just so long, as long as you keep confidence rising. And when confidence reach extraordinarily high levels – the history books are clear – it’s very difficult to increase the confidence further.

2. Investing in 0-rate world

Although there are many arguments why the current valuation might be even low, e.g. discounting future cash flow at a lower rate – I don’t find them appealing enough.

Seen 30 years bonds yield dropping down from 16% to about 2%. In about 2000/2001 those were about 4.1/4.2% and we thought this will be the lowest forever and now it is even lower, and negative all over the world. We have got an artificial interest rate structure, driven down into negative territory, e.g. 20% of government bonds have a negative real return. In other words, you pay to lend them your money, not the other way around.

The same happened with cash – it is deeply negative. Many people literally pay the banks to deposit money, instead of earning anything out of that deposit.

Selling everything in the high will work just fine, however there are major discrepancies as there were in 2000, between US tech, which is overpriced. So, the value of the low-growth stocks is about as cheap relative to the high-growth stocks. All of them are at risk at some degree.

The good news is that oversee they don’t have the same bull market and the same overpricing as we in the US. You can go to the emerging markets – they are not that expensive, compared to S&P they are as cheap as ever could be.

As you won’t be able to make a decent return 10-20 years on US growth stocks (they are heavily overpriced now).

The higher you bid up the price of an asset, the lower the long-term return you will get. There is nothing you can do to change the equation. Every day the market goes higher, you know one thing for sure – that the long-term return will be less than it was the day before.

Growth stocks have outperformed (over the course of the bull market) value stocks by almost 400 basis points. What if, after the bubble pops growth, growth is still ahead and there is no redemption for the value investor? It will be historically unprecedented for that to happen.

“I have no confidence and have not had any for over 20 years in price-to-book and P/E and price-to-cash flow, price-to-sales, even, as a measure of true value. A measure of true value is the long-term discounted value of a future stream of dividends.”

A growth-stock is of course worth a higher ratio than the low-growth stock, but that doesn’t mean they can’t be overpriced. And value should be cheap for what you are. You should build-in the growth, build-in the quality.

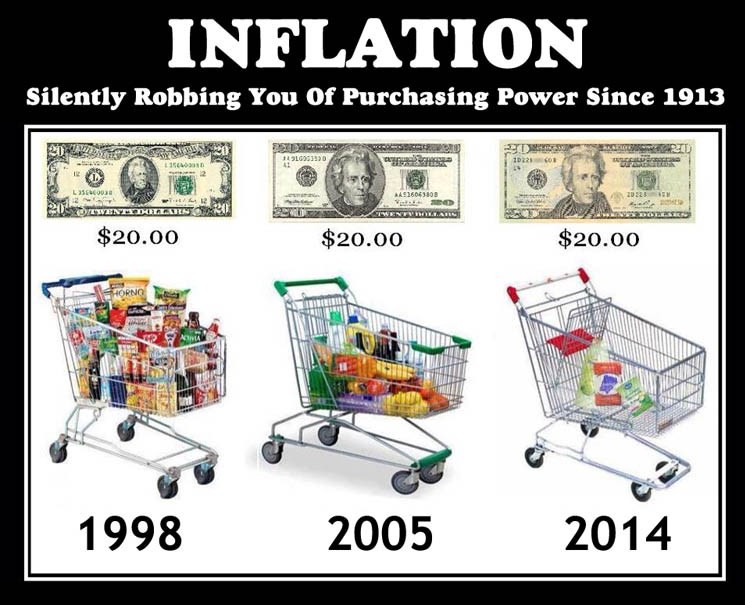

I am also worried about an inflation. We don’t live in a world where output doesn’t matter, and we can just print paper forever. Sooner or later, this will bring huge inflation, that we haven’t seen in 20 years. Everywhere across the globe the price of critical food and metals is going up. Together with the rapidly declining growth rate in the workforce, towards zero and negative.

So, this is a bad time to be caught over speculating.

It is very difficult to allocate in a world of zero rates, stimulus, declining productivity, potential for inflation. Secondly, of course, diversifying – it’s always a huge advantage, and third – the low-growth stocks in the emerging market world are perfectly reasonable if you need to own stocks, and most people do, that would be the way to go.

It will take trillions of dollars to decarbonize the global system – all those companies, doing that, will raise and grow significantly. Those will dominate everyone’s portfolio. Find a good climate change fund and invest into it.

If you think about investing into Bitcoin or any other cryptocurrency – ask yourself – what is the future value of the dividend stream of it? It is nil, it will never pay you a dividend. If you are desperate, can you eat it? Its entire value is on the greater fool. Bitcoin could be worth a million dollars a unit if you find someone to pay it.

And we could think in a similar way about Gold. The difference is that Gold has had a 12,000-year test, and it passed it very well. And Gold also has some other fallback qualities – it doesn’t tarnish, it’s unique, everything ever made of gold is still around and will be around for a very long time. On top of that Gold is heavily used in manufacturing and production of expensive goods and materials. Bitcoin lacks all those.

Bitcoin is 100% faith. Come the next market phase where faith is at a minimum, what do we think will happen to something whose entire reason for existing is faith and nothing but faith?

3. What US government is doing for the economy

Ironically, I believe that Alan Greenspan is responsible for the current situation we are. The FED policy of acting and talking along the lines of moral hazard played a tremendous role.

Alan bragged that he contributed to the strength of the economy through the wealth effect. And there is such effect indeed. If you have the market doubled – 3 or 4% of that gets spent and helps the economy. But the cost of this is tremendous – we live in a real world of people and production and overinflating the value of something does not justify the little growth.

In the end it will all get to a negative wealth effect when the market regulates itself.

Another example are SPACs. Those should be a completely illegitimate instrument. They are just an excuse for people with reputation and marginal ethics to raise a lot of money and take 20% of it for themselves, and a complete rip-off in the sense that the professional hedge funds always liquidate before taking any real risk. And of course, SPACs will make money in the late stages of the bubble, but if you look at the first six years, they had a sub-average return for taking all the risk.

SPACs don’t have enough legal requirements, enough restraints, enough checking. They’re a thoroughly reprehensible instrument and should be disallowed.

The IPO should also be reformed. IPO is a license to reward the fidelities of the world at open. Direct listing made a little easier would be the way to go, but SPACs are terrible.

If you are looking for the very early warning signs of a bubble breaking you find the stocks that have done the best, some particular SPACs, and Tesla, and Bitcoin – and you see that they start to have these big daily drops, and then they recover, and they drop, and they recover.

And the market in 2000 didn’t go together – they took out pets.coms and shot them, the rest of the market continued to go up. Then they took out the junior growth stocks and shot them and the market kept going up, and then they took medium growth stocks and shot them too, and finally by the summer they were shooting the ciscos and the entire tech part of the market. And that had been 30% at the market peak of the total market cap. And yet the S&P by September was at the co-equal high of March which meant that the other 70% had continued to rise.

So bubbles don’t necessarily break on mass, but having sliced off the tech, and the dot coms, then finally the 70% like a giant iceberg rolled over on mass and went down for two and a half years by 50%.

4. US capitalism crisis

The right way to fix the economic inequality is to stop nurturing the moral hazard, and start leading and managing through a monetary policy as opposed to fiscal policy.

By simply pushing up asset prices, you make it difficult to impossible for people to get into the game. The purchase of a house is too expensive, the purchase of anything in stocks is much higher per unit of dividend.

Secondly, the compounding of wealth is reduced. If you have a 6% yield on your assets, you can reinvest them and you can double your money in 12 years. If you turn it into a 3% yield by doubling the price, you are worth more on paper but in real life you only eat the dividends and now they are 3% a year and you double your money in 24 years. So, in 48 years, you are down to a quarter of what you would have been, and so on.

And the gap becomes ruinously wide. The higher the asset price, the lower the rate at which you can compound wealth. And the rich get richer, as you price down the yield, and the poor get squeezed. You are not creating any real value; you are not creating more production and government spending is quite different.

Instead of writing check to everybody, if we write checks for particular infrastructure – we will be doing necessary investing. If we invest into an efficient grid – everybody benefits. So, the Government should come with a strong public spending program, emphasized at the repairing bridges and roads, and green infrastructure, research, training and retraining of people for green jobs.

A corporation in the mid 60s felt it had responsibilities to its workers, it was on the cusp of starting a nice pension fund, a defined benefit. The corporation felt the duty towards the city and the country. All of that is largely gone, but it didn’t go overnight. The idea that the corporation should only care about maximizing profits is a terrible business formula.

If you say as an individual ‘My only interest is to maximize my advantages,’ which is what they say at the corporate level, you are a sociopath. And we are not, as individuals, like that. A lot of us do the odd altruistic act and those are incredibly important in the long run.

Creating a budget and sticking to it is a great way to manage your finances effectively. Here are some steps to help you create a budget and stay on track:

Creating a budget and sticking to it is a great way to manage your finances effectively. Here are some steps to help you create a budget and stay on track: